SaaS M&A Multiples | Exit Planning for a VC backed company

This is the sixth in a series of posts exploring M&A for VC backed companies by Abhinaya Konduru, M25 & Nicole Bentz, Flyover Capital.

Post 1: Why & What?; Post 2: Acquirers; Post 3: Checklist; Post 4: Stories I; Post 5: Stories II

Previously, Nicole talked about why exit planning matters, types of exit paths, types of acquirers, and why companies get acquired. I went through a checklist of items that founders should keep in mind at various stages and some founders’ stories. In this post, we will go into SaaS multiples at the exit.

SaaS M&A Companies

We pulled the data through Pitchbook and looked at M&A deals that took place between 2010 — 2020 with a Valuation / Revenue multiple. This resulted in a total of 219 data points.

Summary:

Valutation/Revenue

What it is: It is calculated by simply dividing the valuation, i.e., the valuation assigned to the company at the exit by the company’s annual revenue at the time of exit.

Why it matters: The Valuation/Revenue multiple is the metric most commonly used when evaluating a venture-backed exit. When analyzing comparable exits in your vertical or industry, this is the metric you will most commonly use to gauge the acquisition price a willing buyer will pay for your company.

Valuation

What it is: The valuation assigned to the company at the time of exit.

Why it matters: This is what an acquirer is willing to pay for your company!

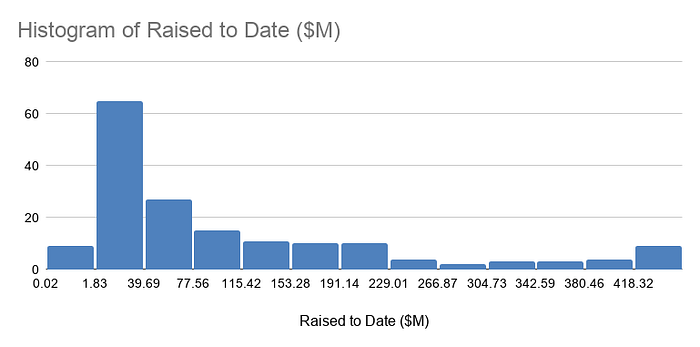

Raised Money

What it is: The amount of capital raised by the company before their exit.

Why it matters: While a company may achieve a huge exit, generating a phenomenal purchase price, if it took a significant amount of capital to reach that exit, it might limit the ultimate return to investors and the founding team. Being able to reach a positive exit while staying capital-efficient, is better than reaching a positive exit but burning through a whole lot of capital along the way!

Years to Exit

What it is: The amount of time passed between the company’s founding and its exit.

Why it matters: The amount of time it takes to grow a company into an attractive acquisition target may or may not be indicative of the purchase price an acquirer is willing to pay for a company. If you recall in our second post, some companies may reach an exit early-on through what’s commonly called an “acquihire.” These exits are usually lower in value but have a higher probability of occurring. Of course, on the other hand, as a company continues to mature it may receive pressure from early-investors to reach an exit.

SaaS IPO’ed Companies

If you’re interested in learning more about comparable public company multiples, check out Jamin Ball’s article. He does a good job explaining metrics and benchmarks examining every SaaS IPO since the beginning of 2018.

Top three metrics, a Saas founder should aim for to go public:

- $200M ARR (minimum $100M)

- 72% gross margins

- 25 months gross margin adjusted CAC payback

In the next post, Nicole and I will go into details about multiples for other business models.